Why you should consider trading grain futures and options.

Commodities have gained a lot of attention over the last several years, with grain markets such as corn and wheat taking center stage following Russia’s invasion of Ukraine. Many traders, investors, and hedgers quickly realized that the war would have a big impact on global production and trade flows (imports/exports) which sent prices screaming higher. Many new market participants are now realizing that

What is a grain futures contract?

Simply put, a grain futures contract is a legally binding agreement for the delivery of grain in the future at an agreed upon price. The two main market participants who use grain futures are hedgers and speculators. A hedger uses the futures market to help manage the risk of adverse price fluctuations. (see example A). A speculator uses grain futures in an attempt to profit from market movements and has no intention to deliver or take delivery of the grain (see example B).

Example A: The Hedger

Old McDonald had a farm, on that farm he grew corn (among all the farm animals). This past spring, he planted 100 acres. With normal growing conditions, Old McDonald estimates that his corn will yield around 170 bushels per acre. The estimated total production for his corn field is 17,000 bushels (100 acres x 170 bushels/acre).

Old McDonald see’s that the price for December corn futures is at $6.00. Old McDonald thinks that is a good price and is worried that the price might be lower by the time harvest comes. Despite the crop still being in the ground, Old McDonald can sell corn futures to help mitigate that risk. Each corn future represents 5,000 bushels (a $0.01 in the market would be +/- $50 for a futures contract). There are also “mini” corn futures, which represent 1,000 bushels. Using his futures account with Blue Line Futures, Old McDonald decides to hedge 10,000 bushels at $6.00 by selling two futures contracts, leaving 7,000 bushels open to price fluctuations (up or down). For each penny the market moves, it will be +/- $100 is Old McDonalds hedge account ($0.01 x 10,000 bushels).

Example B: The Speculator

Sammy the Speculator has been monitoring weather throughout the Midwest this past spring and believes that hot and dry conditions will continue through the summer months. Sammy believes this could lower corn yields in the major producing regions, which could lead to a rise in corn prices. Sammy uses his account with Blue Line Futures to go long one corn contract at $6.00.

Outcome Example 1

In the following weeks, corn price rose $0.50. Sammy is happy with the profit and decides to sell his corn future. Sammy makes $2,500 on the trade ($0.50 x 5,000 bushels).

Outcome Example 2.

In the following weeks, corn prices dropped $0.50. Sammy is afraid prices will keep dropping so he decides to exit his position, losing $2,500 on the trade ($0.50 x 5,000 bushels).

Both the hedger and speculator have the ability to exit and/or reenter positions at any time, during market hours.

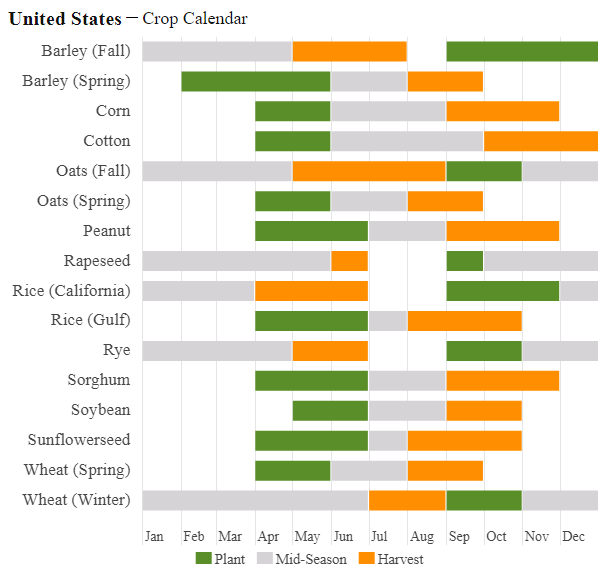

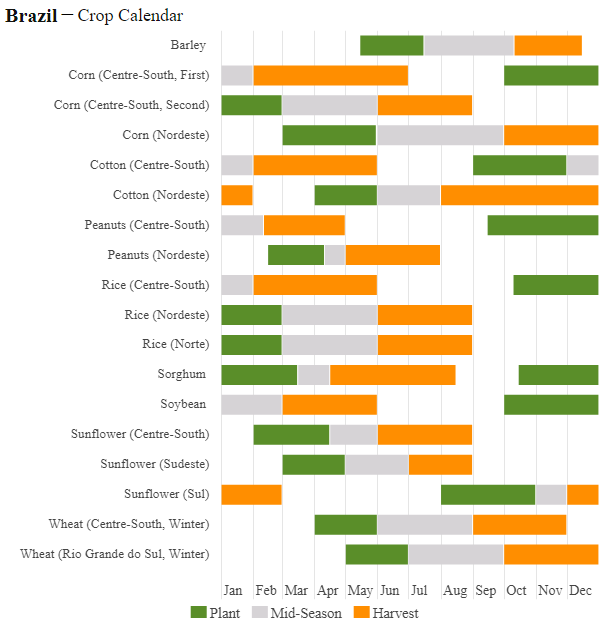

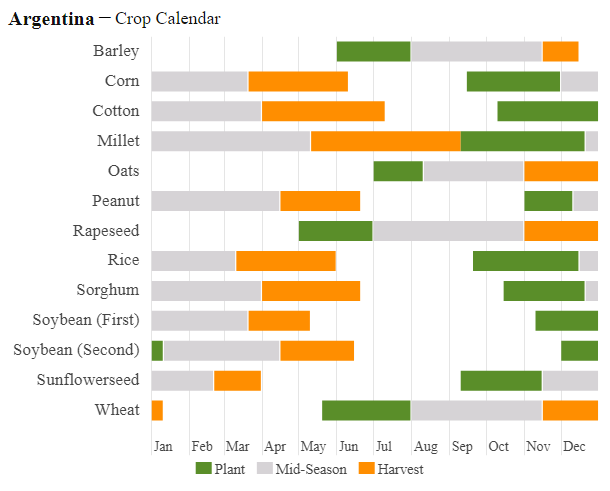

Important Crop Calendars

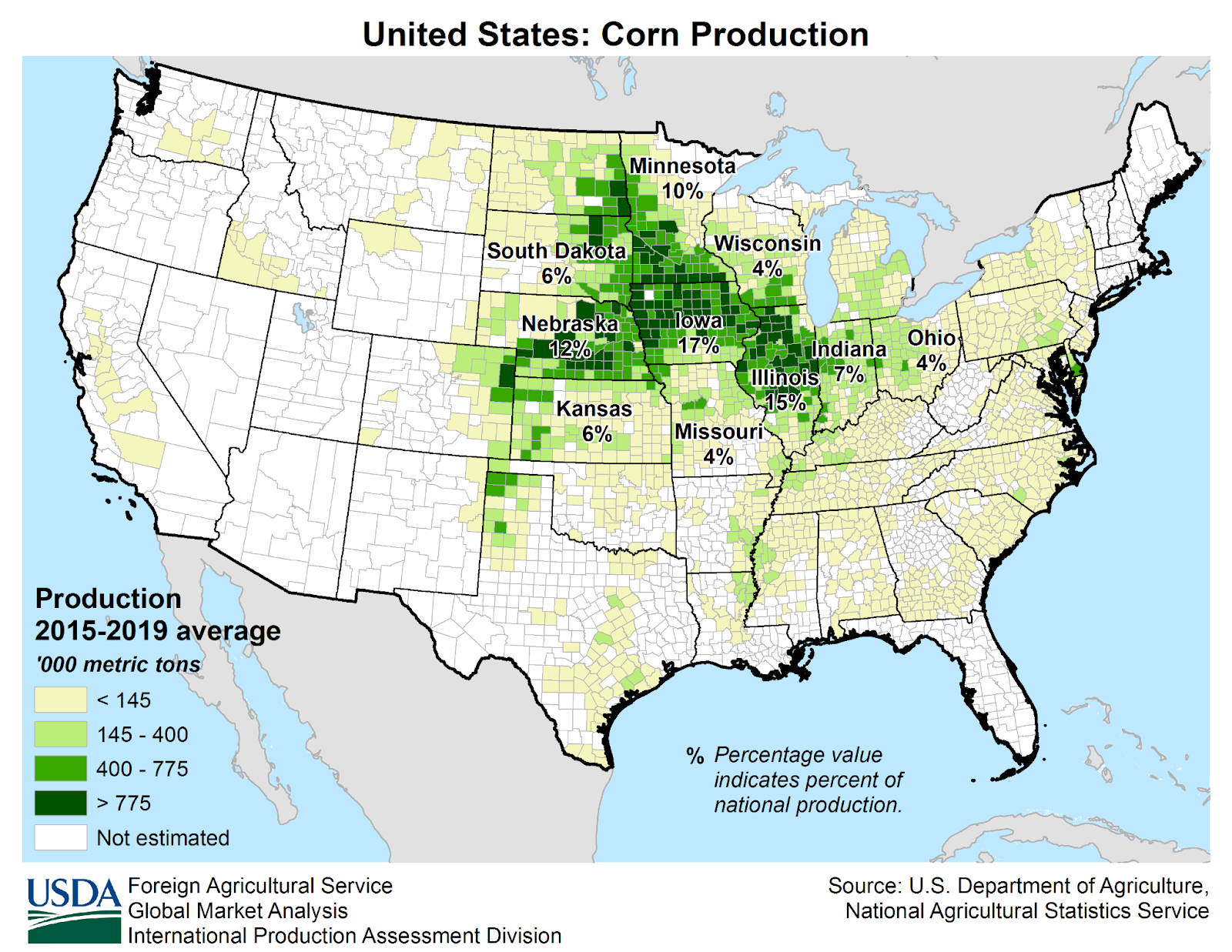

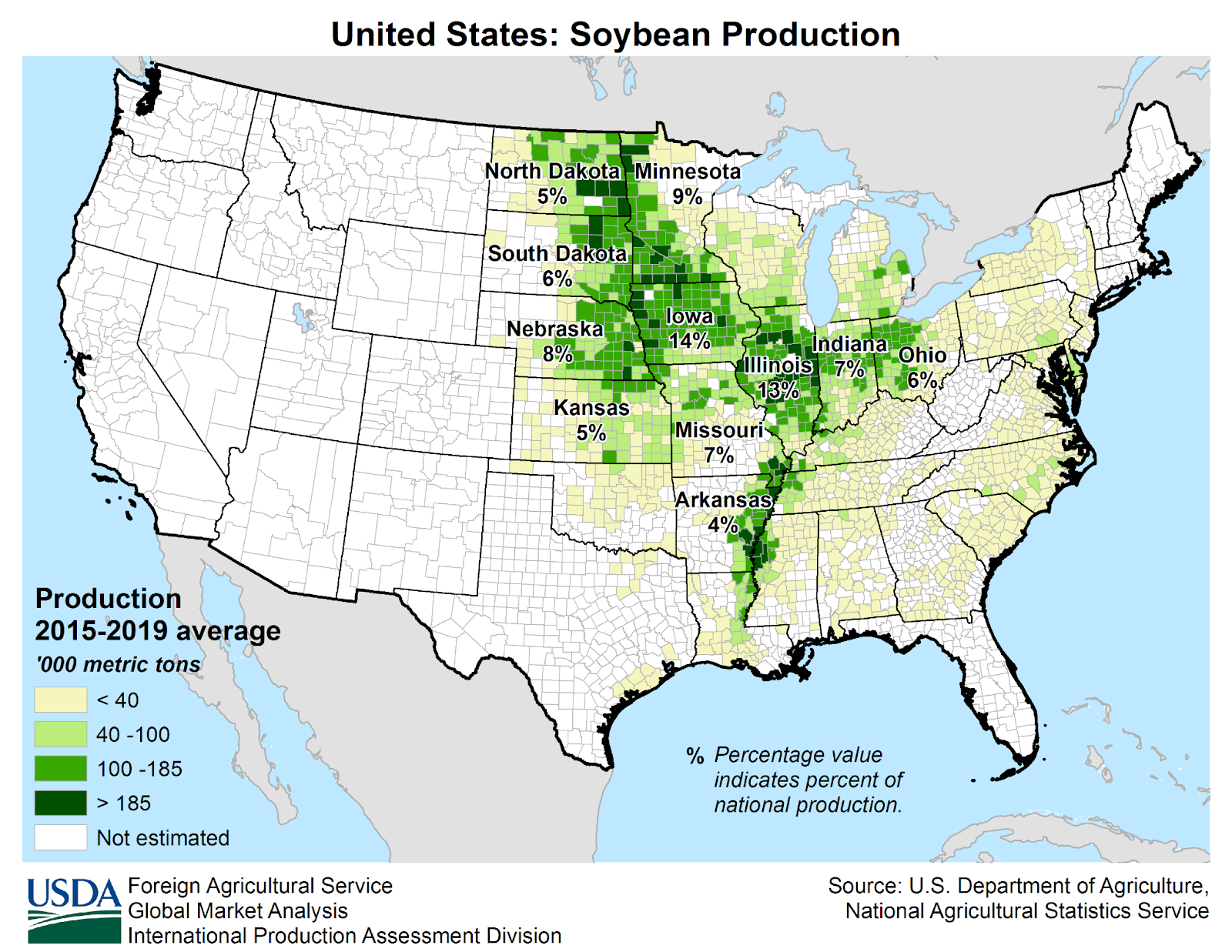

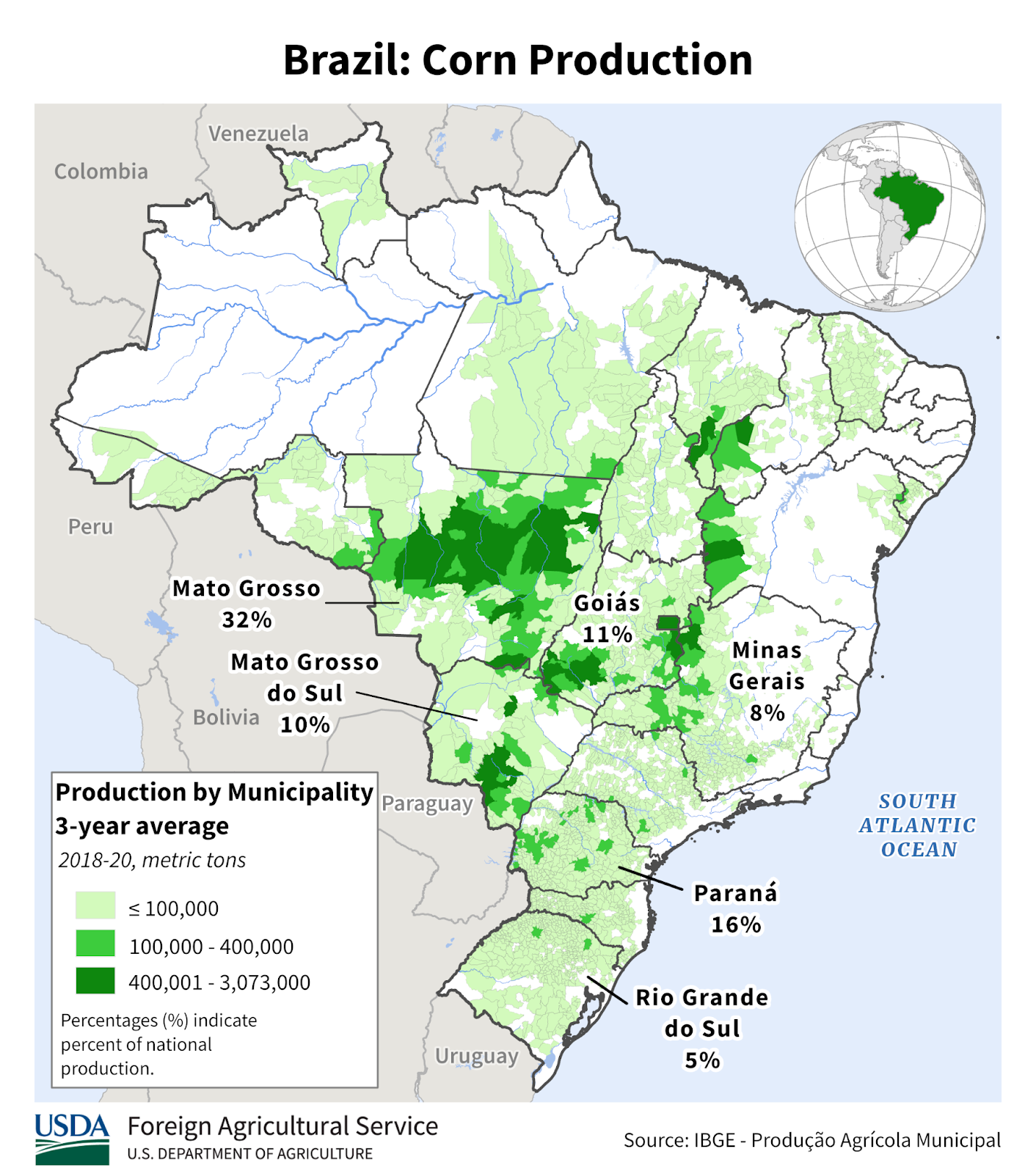

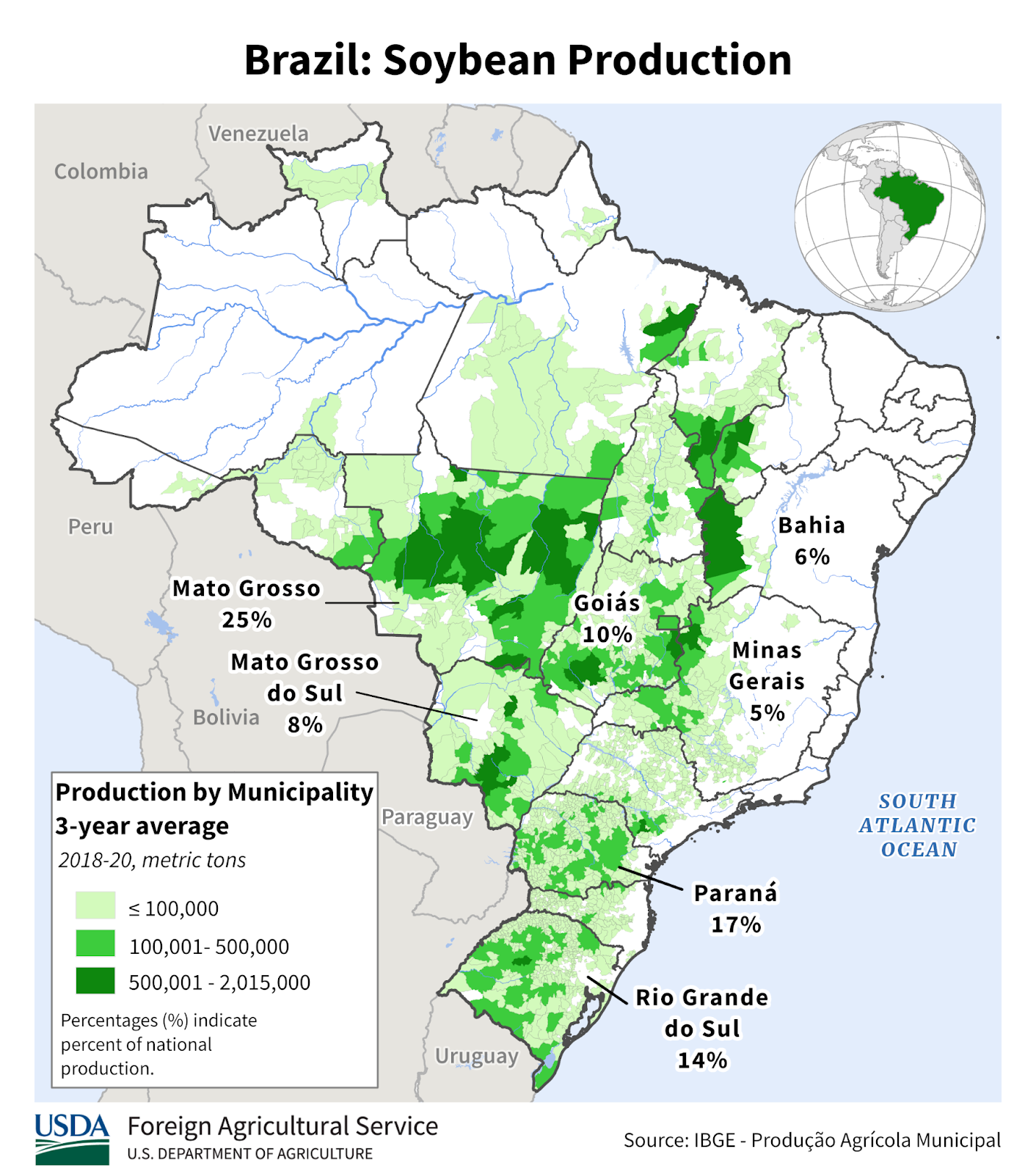

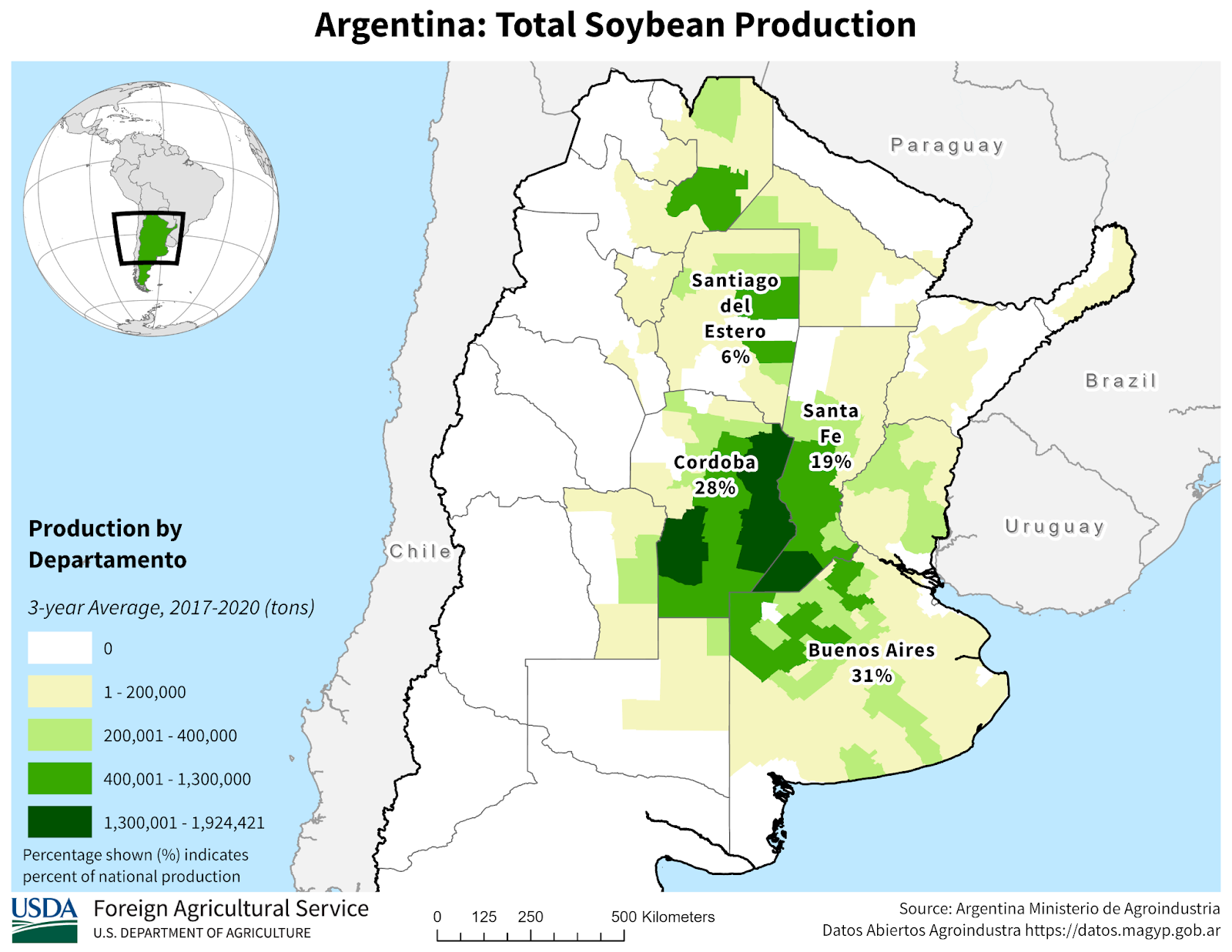

Crop Production Maps

World Corn Production

United States: 30%

China: 24% (they don’t export corn, so it isn’t that important)

Brazil: 11%

Argentina: 5%

Largest Corn Importers

European Union: 12%

China: 10%

Mexico: 10%

Japan: 9%

Largest Corn Exporters

United States: 29%

Brazil: 26%

Argentina: 23%

Ukraine: 10%

World Soybean Production

Brazil: 39%

United States: 30%

Argentina: 13%

Largest Soybean Importers

China: 59%

European Union: 9%

Largest Soybean Exporters

Brazil: 53%

United States: 33%

Argentina: 5%